Quick Summary

- Energy prices rose sharply in March following energy supply disruption in the Middle East.

- EV fleets can still capture low power prices with the right flexibility.

- Renewables are creating more low-price periods, while gas is driving higher peaks.

- Smart charging and optimisation are becoming more valuable for controlling fleet costs.

Why flexibility and smart charging matter more than ever

The conflict in the middle east and the de facto closure of the Strait of Hormuz, which began on 28th Feb 2026, resulted in energy prices soaring. A useful way to see how prices changed is to consider how the price of GB baseload power for delivery in April increased. During the first 3 weeks of February the average closing price for April power was £71/MWhr, whereas on average during March the price was £96/MWhr, an increase of 37%. Despite the temporary cessation of hostilities, these risks remain.

While the cost of energy increased across the board, opportunities remain to capture low prices if you have a degree of operational flexibility, visibility of market prices, and a power contract which gives you market access.

Two trends are evident which enhance the opportunity to capture low prices.

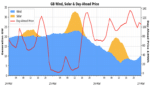

#1: the influence of renewable energy production on the power market price

We see this trend in GB and in many other countries, where renewable energy production has a growing influence on wholesale power price – this trend has been coming for multiple years, but the current energy crisis is exaggerating it. In GB, the bifurcation between periods where wholesale electricity prices are set by renewables and periods where prices are set by gas has become even clearer due to the conflict.

The period from Tuesday 24th to Thursday 26th of March in GB is a good example and is shown in the graph below – wind and solar generation was forecast to be high on the 25th pushing the day-ahead price very low during the day to between 0 and 30 £/MWhr. In the late afternoon and evening, renewable generation was expected to fall away rapidly by more than 15 GW, which pushed day-ahead prices up to over £125/MWhr. This is an example of the market switching from prices being set by renewables, to prices being set by gas generation.

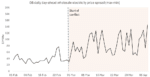

#2: the increase in daily price spread as the market for gas has tightened

The daily price spread, the difference between the maximum and minimum price in a 24-hour period, tends to increase when there is a scarcity of supply. Rising gas prices, and therefore wholesale electricity price (when renewables production is low), results in higher peak prices relative to the average. So, even though the whole market has risen due to the ongoing conflict, the daily variation has increased, creating a wider absolute spread between min and max prices. Additionally, with the growing penetration of solar generation, double peaks and troughs within a 24-hour period are now commonplace, with both morning and evening peaks, and daytime and overnight lows.

The graph below shows that during February, the average daily price spread (using GB day-ahead wholesale electricity prices) was £38/MWhr, rising to £83/MWhr in March. While some of this increase is due to greater within-day solar generation in March relative to February, much of it is driven by higher evening peak prices linked to gas costs, alongside periods of strong wind generation delivering very low prices.

What this means for EV fleet customers:

Together, these two trends mean that the opportunity created by wholesale electricity price variability has increased significantly, along with the risk of hitting very high prices – the highest day-ahead price in March was £189/MWhr, whereas the lowest price was £(1)/MWhr.

VEV’s customers on day-ahead cash-out products, optimised through our VEV IQ platform, saw much more modest increases in electricity costs in March than the wider market increase might have otherwise suggested. This has been achieved through a combination of operational flexibility and VEV IQ controlling when charging takes place within operational constraints. While overall market prices have risen, the spreads between low and high prices still create significant opportunities to minimise costs, provided the right tools are in place.

Please reach-out if you would like to learn more about VEV and our energy procurement and optimisation solution.

8 April, 2026

Sources: Elexon; Energy Quantified